Triple entry accounting : One of the greatest inventions in the last few centuries in the world of accounting

Overview

Currently global accounting practices/accounting standards and related technology solutions are built on top of a fundamental accounting principle known as double-entry bookkeeping. In the double-entry accounting system, at least two accounting entries are required to record each financial transaction.

In recent times, I believe that the limitations of these principles have led to rise in frauds and increasing dependency on the auditors to establish the accuracy of the entries. Time is apt for re-assessing the way the entries for all transactions are recorded and processed with a focus on building trust within the process and systems rather than putting undue pressure on regulators, auditors and assessment services.

In my opinion, one of the solutions is to use triple entry accounting. This is an enhancement to the traditional double entry system in which all accounting entries involving outside parties are cryptographic sealed by a third entry. However, there has to be a conscious move to technology and systems which enable triple entry accounting. Undoubtedly, The benefits overweigh the transformation challenges. By making use of the immutable data on a real time basis which can be assessed and incorporated into the decision making process, following use cases can be achieved:

Government bodies can use this technology innovation to facilitate diplomatic decisions in the global trade process and ease out the process of import and export documentation and delays associated with trade.

E-invoicing and instant reporting of invoice by mandate can be considered as the first step towards triple entry bookkeeping where government tax departments act as the guardians of immutable ledger. In my opinion, this will usher in trust and reduce the chance of frauds not only with the participating parties in the trade but with the entire economy itself.

Tax administration would be positively impacted where existing self-assessment will transform to tax determination. A combination of hardware and software enabled with the latest triple entry bookkeeping principles will help compute tax consequences and deliver tax receipt to the taxpayers like a postpaid mobile phone bill. Similarly, a refund voucher/note will be issued in case of excess credit with the Government.This will contain all taxable transactions so that taxpayers can pay their tax obligations without the need of filing a tax return.

Double Entry Accounting/Bookkeeping

There is a bit of confusion on the actual date or events which lead to double entry book-keeping taking centrestage. Based on some of the articles that I have read, double entry practices originated in Italy in 1211 AD where a bank in Florence used the system for managing their internal accounts. It became popular after 1490’s when a Venetian mathematician Franciscan friar Luca Pacioli published a book, Summa de Arithmetica, Geometria, Proportioni et proportionalita (Sum of Arithmetic, Geometry, Proportion and Proportionality). It originated at a time when humans were using paper based systems to record and transact data.

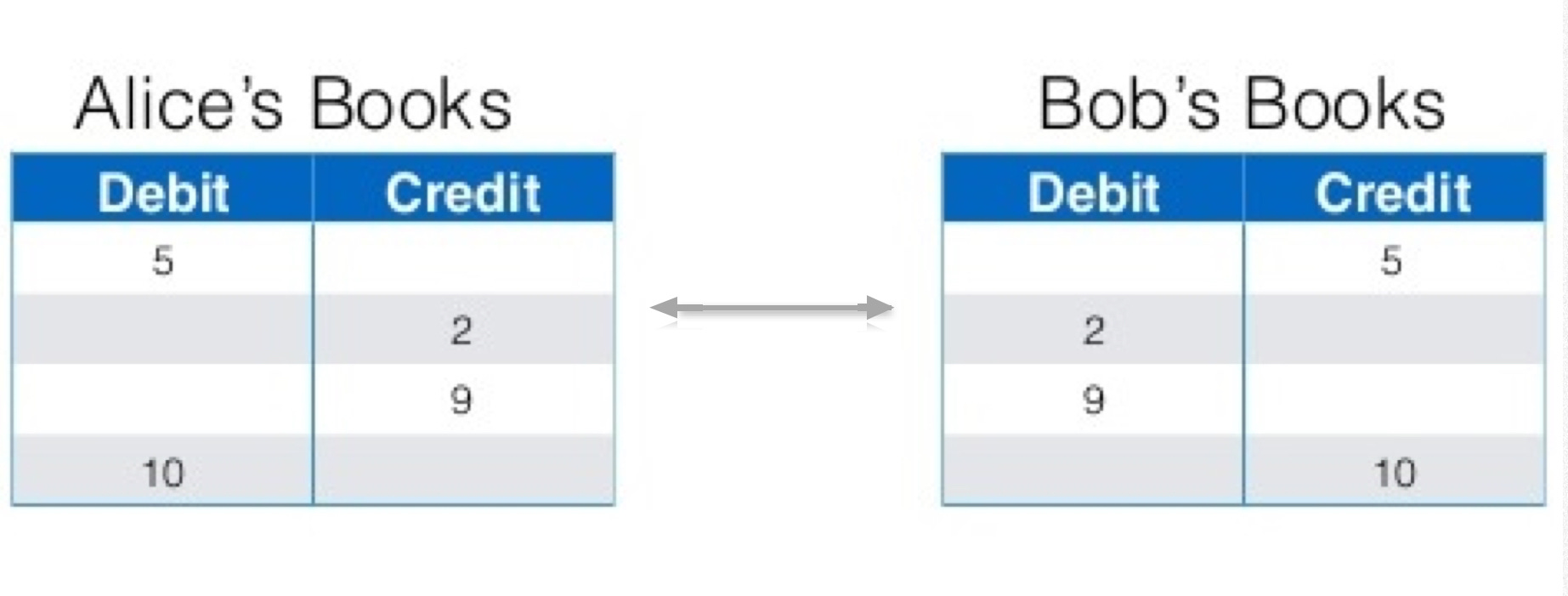

Below is a visual representation of double entry bookkeeping where Alice and Bob engage in transactions with each other. Every transaction linked to one side of the account requires a corresponding and opposite entry in the account on the other side of the transaction. The double-entry has two equal and corresponding sides known as debit and credit.

Double entry was effective for cross checking transactions and establishing trust and transparency between participating parties. But the associated stakeholders such as investors, auditors, tax authorities and financial institutions, are at the mercy of information disclosed by the participating parties. For e.g. auditors need evidence to ascertain that 5 has been debited from Alice’s book and credited to Bob’s book because there was a transaction between Alice and Bob. There has to be an assessment on both sides of the transaction with paper trail or digital documentary evidence such as invoices, payment orders, actual payment receipts and such evidence. This is a fundamental limitation. Because there is a chance that the disclosed information is not accurate or consistent as the evidence can be falsified in most cases. Though assessment techniques have advanced over time, there are chances of process inefficiency and manual work required by finance professionals such as manual reconciliations, data omissions and manual errors due to the fundamental limitation of this accounting process. Internal controls of the organizations too have to be strong to avoid such frauds especially as there is a reputational risk for participating entities other than civil and criminal proceedings in some cases.

The self assessment tax compliance process is also built up on double entry accounting principles. Fraudulent entities have been known to use the limitations as a loophole by falsifying the transaction volume, indulging organised financial crimes and disclosing fake transactions which cannot be currently prevented due to lack of relevant capacity or capability. Though there has been a conscious attempt to build both capacity and capability, it might take longer than expected without moving to triple entry accounting.

Currently, auditing is the only way to find out the defaults after the transaction has happened which again have been known to be prone to manual errors and frauds. Organised financial crimes in association with auditors have risen even though there has been higher vigilance and reviews from regulatory authorities. Wirecard fraud is one of the recent examples.

Triple entry accounting

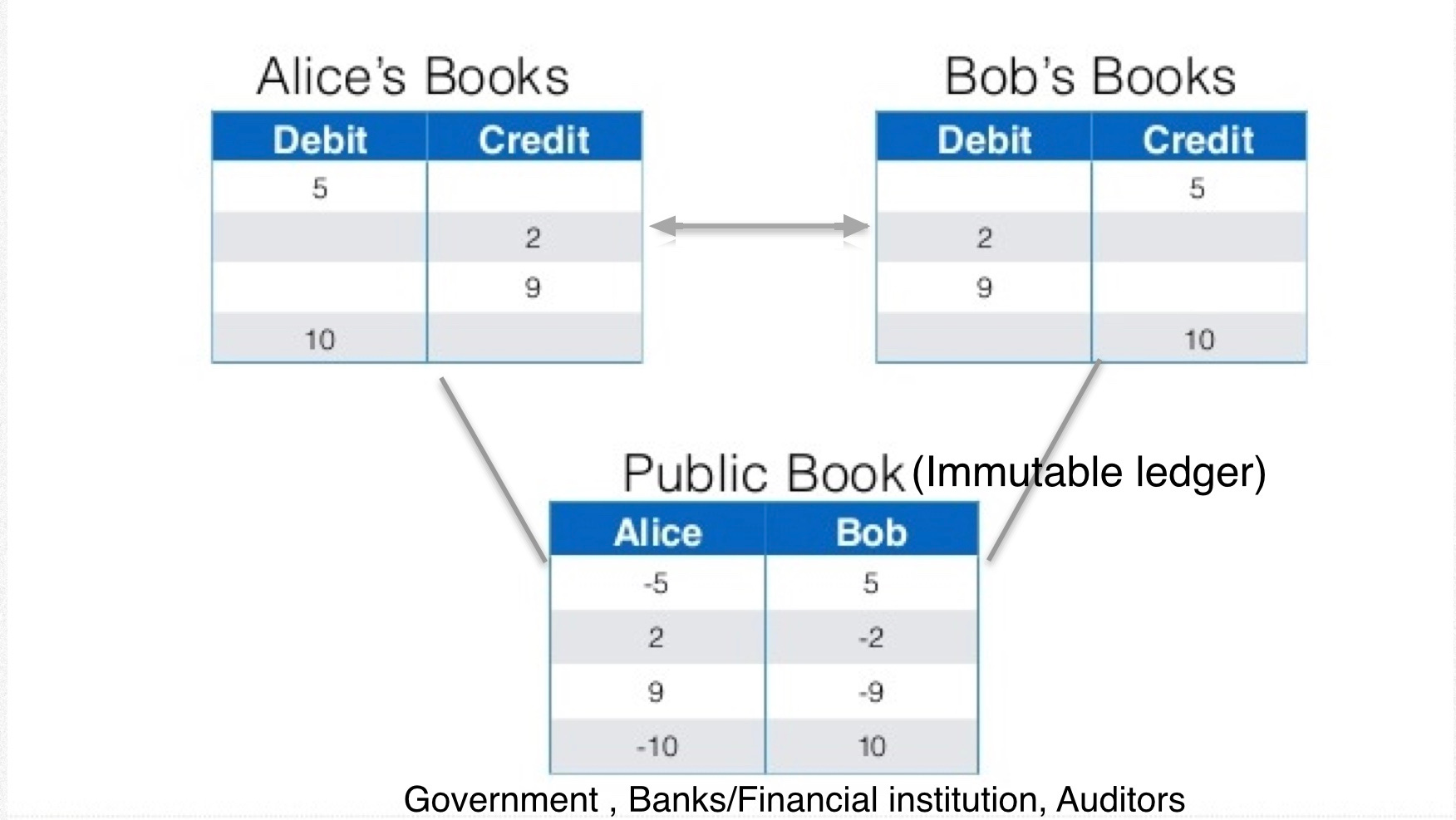

Triple entry accounting system tries to overcome the limitations of the double entry accounting by creating a link between the two double entries and one entry recording it in an immutable book/ledger. The transactions are recorded in three different books/ledgers (hence the name) by both participating parties as well as a common ledger (usually cryptographically secured) or public book. A central government agency can be the guardian of this immutable ledger or public book, especially for public data such as trade transactions and resultant tax. If the implementation is done properly, there might not be a need for any external auditors for these records as they have to be auto-reconciled for e.g., a transaction between Alice and Bob has to generate a digital payment invoice which can be read through an OCR and validated automatically along with the actual payment reference number provided by the transacting banks.

Following is a visual representation of triple entry accounting with same example of Alice and Bob

Some of the parameters which can be considered as the data elements for recording these transactions would be:

Digital or paper-based invoice (e.g. those generated manually or by the ERP systems of the companies)

Payment order

Actual payment reference number from participating banks/FIs/payment gateways

Tax registration numbers of entities (e.g. TIN, PAN etc.)

Aadhar IDs of individuals responsible for transacting

Audit trail - date, time, location (perhaps GPS), email ID, phone numbers

Digital signatures

Tax calculation on the transaction - for e.g. GST paid by Alice/Bob

Transaction details - for e.g. purchase of raw materials or sale of manufactured goods

Any other which would help uniquely identify and authenticate the transactions

To capture the above data elements would need considerable change in the policies, systems and processes currently utilized and would need strong collaboration of all stakeholders - public and private.

The Bitcoin network (with underlying blockchain technology) can be considered as the first successful implementation of triple entry accounting in the financial industry. It is a growing record of transactions which provides trust and transparency to every party in the network so that the network can automate the auditing process on a real time basis and nobody in the network will be able to lie/falsify data regarding the transactions.

We can add the significant use cases in finance and audit industry which are currently in practice,where triple accounting system is implemented (Refer Inter.x), also Coca Cola Supply chain reconciliation concept.

Blockchain technology enables triple entry bookkeeping. A common entry is made using an immutable ledger which cannot be corrupted by any party including the administrator of the network. External stakeholders can have trust and transparency with transactions and they are no longer at the mercy of the participating parties for information disclosure. This subtle change in accounting practice will have a butterfly effect on the entire economy.

Fraudsters exploiting the loopholes of double entry accounting will no longer be able to manipulate transactions already registered over the ledger and this will ensure integrity that they should have inherently possessed without supervision. The current post transaction auditing will transform to real-time transactions auditing thereby reducing the risk associated with auditor frauds.

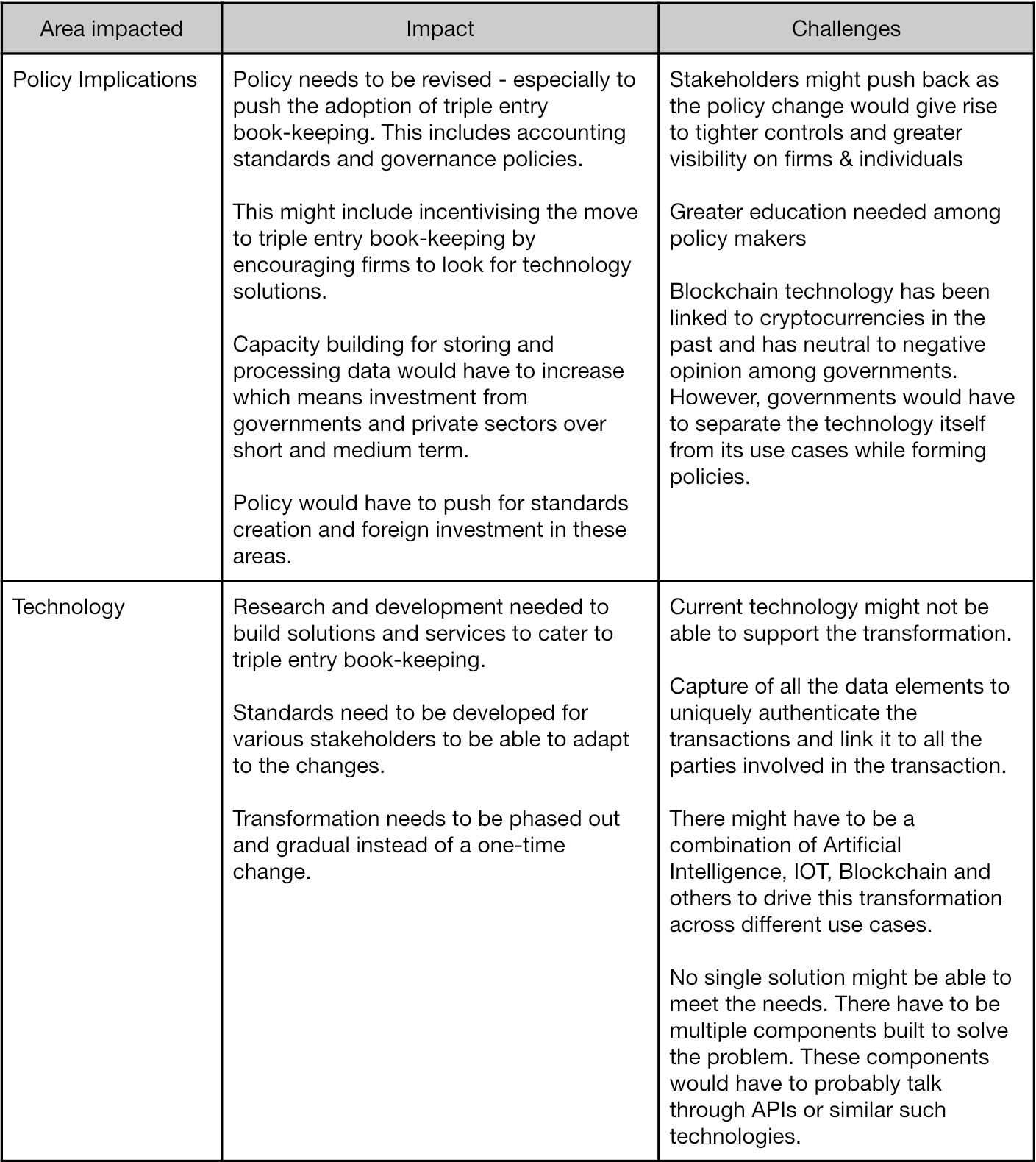

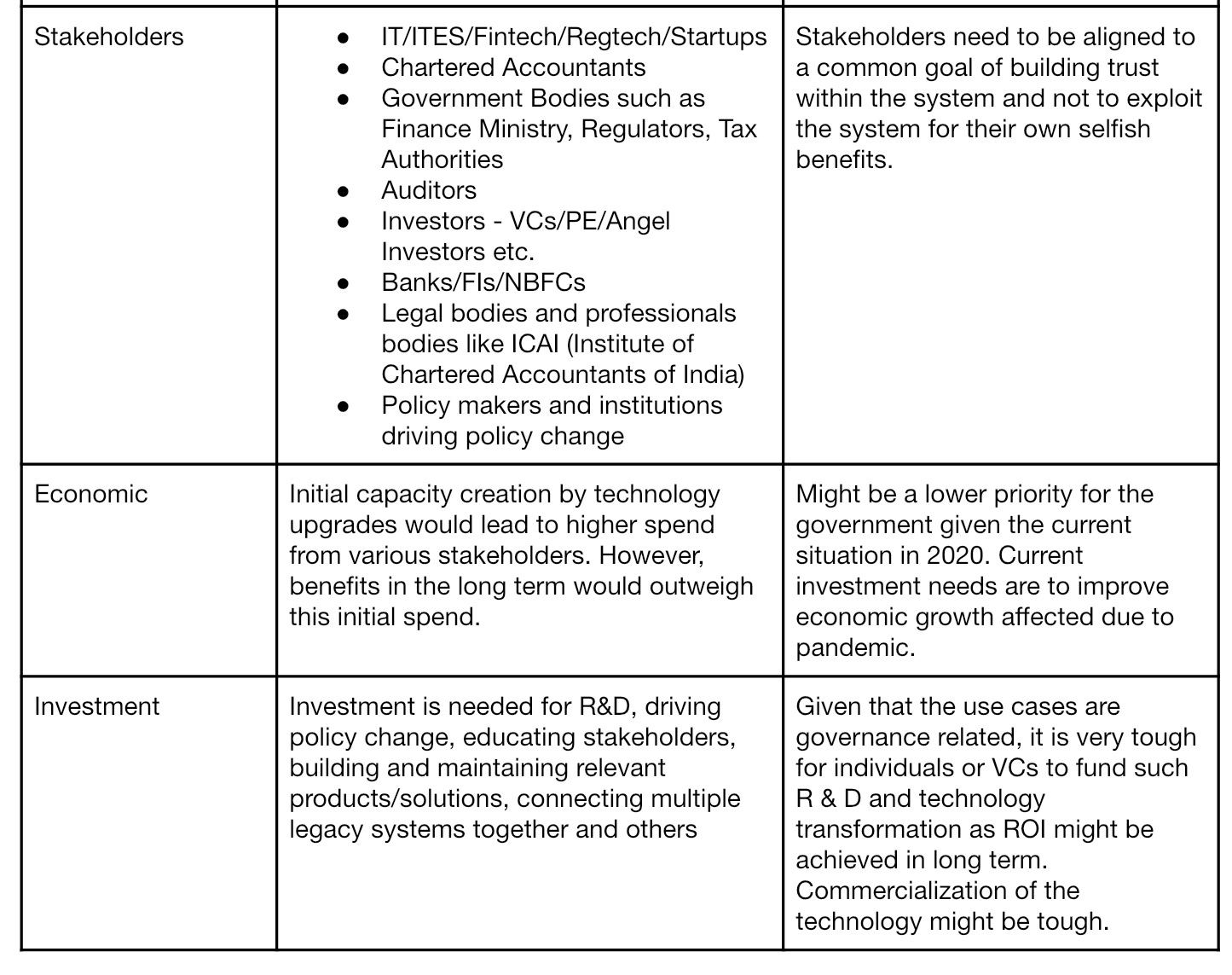

Impact and challenges

Government of India’s NITI Aayog has studied the benefits of blockchain technology in their study paper titled ‘Blockchain: The India Strategy’. There is a mention of blockchain and its utility for decentralized systems plus entity-less trust systems. However, NITI Aayog also has mentioned about the hype of blockchain technology as a ‘silver bullet’ to solve all problems. It talks about the utility of blockchain in improving processes than being used as a new approach to solve the problems. I believe this paper is quite important to be read and understood to be able to solve problems faced by the government. To solve the problems, blockchain technology should be viewed as one of the missing pieces of the jigsaw puzzle, rather than trying to solve the entire problem just with blockchain technology. Some of the concepts utilized in blockchain technology such as cryptography, decentralization, game theory etc. can be incorporated to solve the problem rather than perhaps investing time and effort in creating new blockchain protocols and pushing for its adaptability which might not be practical.

The transformation to triple entry book-keeping will have its share of challenges.

About the author

Sooryanath is the Co-Founder of Spathion (www.spathion.com). Spathion is an innovation think tank and technology solution and services provider. It provides free and easy infrastructure for professionals to learn and implement a triple entry accounting system in their everyday work. Spathion wants to provide solutions with the purpose of innovatively solving problems faced by governments and organizations.

Soorya is leading the Smart Economy working group hosted by Government Blockchain Association USA.

He can be reached at soorya@spathion.com.

References

Ian Grigg, ‘Triple Entry Accounting’ - https://iang.org/papers/triple_entry.html

https://systemsinnovation.io/triple-entry-accounting-articles/

https://blog.goodaudience.com/blockchaintech-can-triple-entry-accounting-save-the-world-896092da4694

https://niti.gov.in/sites/default/files/2020-01/Blockchain_The_India_Strategy_Part_I.pdf